Embedded insurance partnerships in 2026: from linear deals to ecosystem orchestration

In a nutshell

- Bespoke partner integrations that take 12-24 months prevent carriers from scaling embedded insurance programs

- Embedded insurance ecosystems let carriers, distributors and tech partners collaborate via APIs without rebuilding everything.

- Modular platforms cut integration time from years to weeks using configurable components.

- Orchestration is the new advantage: carriers who master platform orchestration will unlock new distribution channels and revenue streams.

Jonas von Oldenskiöld is Head of Partnerships at Qover, where he drives strategic collaborations with insurers, banks and brokers. With over a decade of international leadership experience across Europe and Asia, Jonas has successfully led P&L operations, market expansion and large-scale transformation initiatives.

At Qover, he empowers partners to harness the full potential of embedded insurance through a modular orchestration platform for seamless, tech-enabled insurance experiences across borders.

Remember when B2B was ‘simple’? Seller calls buyer. Buyer signs contract. Everyone goes home happy. Those days are long gone my friend.

The good ole’ linear model has broken apart. With AI reshaping everything and buyer journeys fragmenting, the 'full-stack' solo act no longer works.

The reality is that no single company can provide the entire value stack anymore.

We've moved into an ecosystem-led model where winners aren't those who own every asset – they're the ones who master partnerships and build adaptable ecosystems ready for whatever comes next.

The shift from transactional to embedded insurance partnerships

We can't afford to think linearly anymore. Still building bespoke integrations for every partner?

Those 12-24 month projects aren't just slow; they're actively killing your ability to compete. While you're deep in Year 2 of a custom build, your competitor has onboarded 15 partners using APIs.

These bespoke builds are silent killers, locking companies into cycles that prevent them from moving toward true platform orchestration, and instead focus on managing complex never-ending projects, with little new business generated.

I've lost count of how many times someone's told me 'insurance is too complex to move fast.'

But when I look at what carriers are actually doing – adapting to cyber threats that didn't exist five years ago, responding to climate risks in real time – that doesn't sound slow to me. The problem isn't the industry, but rather the infrastructure.

.jpg)

The embedded insurance space in particular is facing major change, driven by new distribution models, real-time data and API-first platforms.

The numbers are pretty hard to ignore. The embedded insurance market is set to grow from around $144 billion in 2025 to over $1.4 trillion by 2034. More than 75% of the market is already online and API-led, growing at 20%+ annually.

To capture this growth, we need to shift from product to outcome:

- Stop building silos: multi-year transformations bring high execution risk and opportunity cost

- Start building portfolios: use ready-made modules for quote/bind APIs and claims automation instead of rebuilding from scratch

- Own the architecture, not the assets: create a 'technology shelf' – reusable components and integrations that partners can easily access and benefit from

Think of it like IKEA (I'm Swedish, so this analogy is mandatory). They don't build 20 different wardrobes from scratch. They build one solid base, then let you choose the shelves, doors, handles and finishes that work for you.

Embedded insurance should work the same way. The orchestration layer is your configurable system: same core infrastructure, endless combinations. Partners get exactly the coverage they need without rebuilding everything from zero.

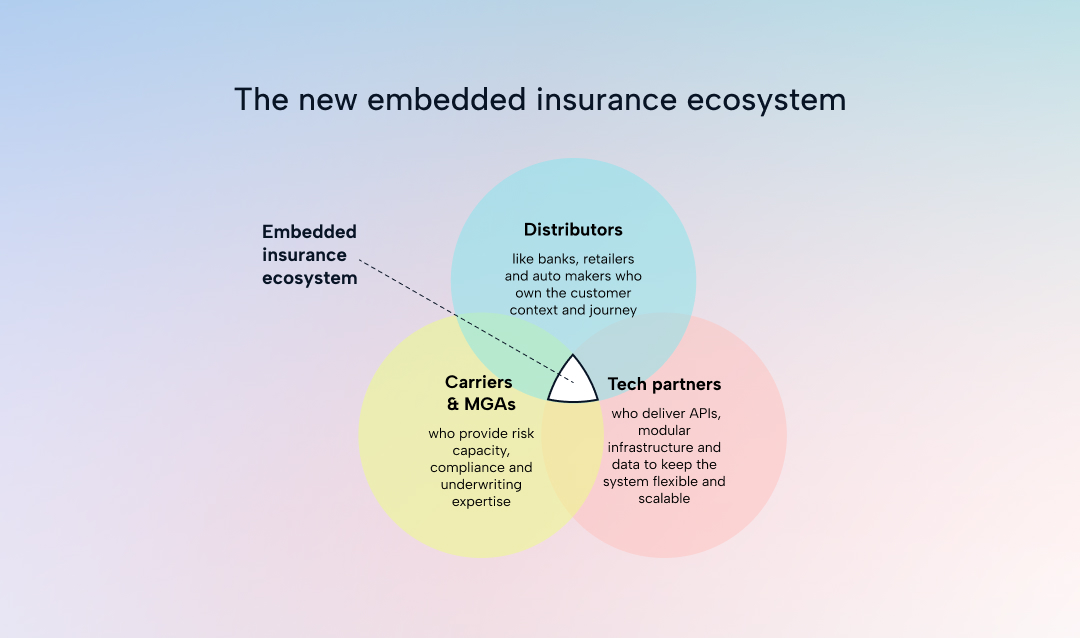

How embedded insurance ecosystems actually work

Embedded insurance shows how expertise should be exchanged, not rebuilt. Success depends on three main types of collaboration:

- Distributors (banks, OEMs, retailers, platforms) who own the customer context and journeys

- Carriers & MGAs who provide risk capacity, compliance and underwriting expertise

- Platform/tech partners who deliver APIs, modular infrastructure and analytics to keep the system flexible and scalable

Strategic insurtech partnerships play a critical role in making these ecosystems function effectively.

But the ecosystem doesn't stop there. Other service providers – from data and analytics firms to assistance and value-added services – enrich this network with additional insight and utility.

Here's what this looks like in practice: a neobank uses their customer data and interface, pulls underwriting from a carrier and leverages a platform for the API infrastructure and claims automation. None of them have to build the full stack, so all of them win.

Each player focuses on their core strength while exchanging capabilities per use case, without rebuilding the entire stack every time. This isn't just theory; insurers who embrace ecosystem thinking can unlock new revenue streams and access customer contexts that were previously out of reach.

Why adequacy, not just access, will define the future of embedded insurance →

Why modular insurance partnerships scale faster than bespoke

The future isn't custom code – it's configurable building blocks. By using reusable, parameterised components per partner, we create an ecosystem where participants can be added, scaled or swapped without rewriting everything.

The difference is huge. Modern embedded players report integration times measured in months, not years, using unified APIs and modular 'product shelves' that partners can configure rather than custom-build.

This shift requires insurers and brokers to embrace orchestration rather than trying to build every capability themselves. Instead of 12 to 24-month projects, winning platforms enable partner onboarding in a matter of weeks.

In a world of trust fatigue and constant change, a validated ecosystem becomes one of your strongest assets. Today, it’s a must-have. The carriers and distributors winning in embedded insurance aren't the ones trying to do everything themselves – they're the ones who figured out that orchestration beats ownership.

The question isn't whether you should partner. It's whether you can afford to wait another year while your competitors build ecosystems that leave you behind.

.jpg)

.webp)

{kind=link}

{kind=link}