In a nutshell

- Insurance-as-a-service (IaaS) is transforming the industry, delivering more accessible, digital-first insurance embedded into everyday experiences.

- For brands, it opens new revenue streams, boosts customer loyalty and speeds time-to-market with tech-first infrastructure.

- For insurers, it provides modern distribution channels, streamlined operations and scalable growth.

- For consumers it offers relevant, transparent cover at the right moment, with smoother claims and better support.

Alex is in charge of content marketing at Qover, meaning she's obsessed with all things storytelling and tone of voice.

With more than a decade of experience in content strategy, copywriting, editing and SEO, she's worked for media companies, marketing agencies and startups across the globe.

When she's not writing or strategising, you'll likely find her in a language class (Dutch, currently), on a spin bike or diving into her latest Netflix binge.

For decades, insurance has endured a laggard reputation. Slow, clunky, behind the times. But the industry is finally catching up, thanks to a wave of digital-first models that make insurance faster, fairer and easier to access.

Today, this shift has a name: insurance-as-a-service (IaaS). And it’s changing how businesses launch and manage insurance products.

Whether you're looking for an insurance platform as a service, a flexible insurance SaaS solution or modern digital insurance solutions in general, the goal is the same: embed coverage seamlessly into your customer journey, without the usual complexity.

The rise of insurance-as-a-service: why the industry is going digital

Digital services are no longer a nice-to-have. The frictionless user experiences that many have come to expect have raised the bar for customer expectations across industries – including insurance.

This has led to a reimagining of the insurance value chain, leveraging previously unexplored capabilities to produce a new type of digital insurance: cover that prizes transparency over opaqueness; mass availability over limited access; and streamlined efficiency over a painfully slow process.

Like banking-as-a-service and software-as-a-service, insurance-as-a-service emerged to fill this gap, offering simpler, scalable insurance products embedded into everyday digital experiences.

What is insurance-as-a-service?

Insurance-as-a-service is a business model where companies – often insurtechs and insurance providers – offer digital insurance products and services to other businesses, rather than going directly to consumers. This makes it easy for non-insurance businesses to embed insurance into their existing platforms and customer journeys.

It’s a fully digital insurance offering that can cover end-to-end requirements for simpler distribution, claims management, customer support and more. It’s also commonly referred to as ‘embedded insurance’, which is seamlessly built into a product or service at the point of need.

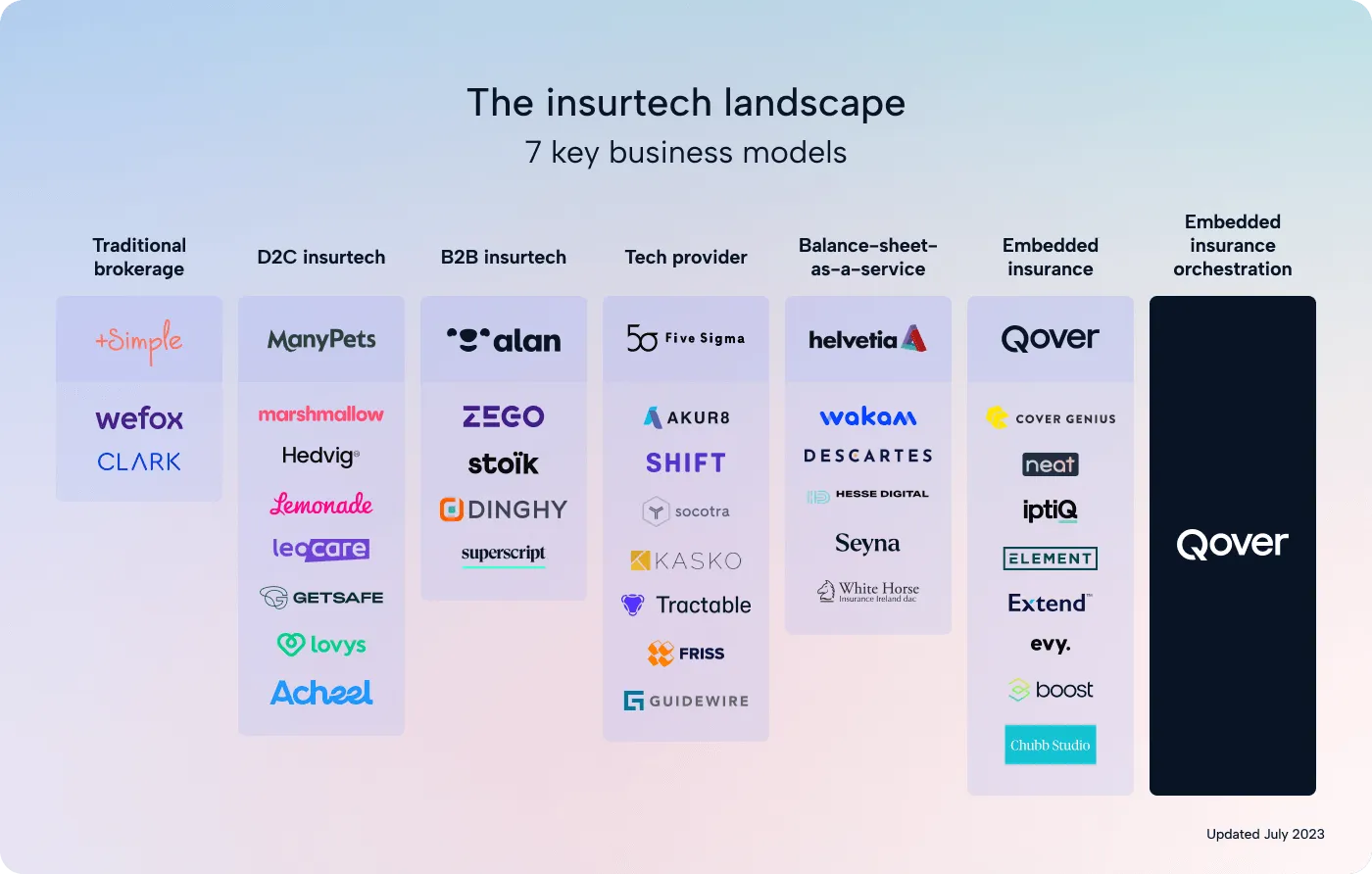

While there are several different types of insurtech business models, increasing number of insurtechs see themselves as orchestrators, going a step further to call their services ‘embedded insurance orchestration’. These players do more than deliver an insurance SaaS platform; they also facilitate the other parts of the value chain that make insurance so complex, like compliance, pricing and data.

%20(1).jpg)

With an insurance SaaS platform, companies can pick and choose the insurance components they need. So rather than building the insurance operations and technology in-house, they can partner with an IaaS provider. This offers a range of benefits to the companies – from flexibility to increased revenue – while also creating a more seamless experience for end customers looking to buy insurance or file a claim.

Traditional insurers can also benefit from partnering with embedded insurance providers. Since many risk carriers have been around for decades, updating their current infrastructure to fit the digital age is complex and expensive. By pairing up with insurtech providers, risk carriers can create a better experience for the customers they serve.

‘Embedded finance in the broader sense has been around for many decades’, says Timm Schipporeit, Partner at Perella Weinberg Partners. ‘But what is really different today is the technological sophistication, the modularity by which it can be provided and the ease of integration. It used to be very monolithic. Companies were usually partnering with one large provider who could do all of that, but in a very inflexible way.’

‘What we’re seeing today is seamless integration between insurance and software platforms and marketplaces, thereby enabling minimum friction and ultimately a better proposition that drives customer experience, increases access to financial services and reduces the cost for the consumer.’

Read more about the 7 key insurtech business models →

How an insurance platform as a service works

An insurance platform as a service delivers the technology and orchestration needed to embed insurance seamlessly into a digital journey. Rather than building complex systems in-house, businesses connect through APIs that handle distribution, claims, pricing flows, reporting and customer support.

Key features include:

- APIs for integration: embed insurance directly into apps, checkouts or digital journeys.

- Regulatory support: stay aligned with local and international regulations.

- Data and reporting infrastructure: access real-time insights on performance, claims and customer behaviour.

- Scalable, modular design: choose the components you need, whether that’s customer support, claims handling or orchestration across risk carriers.

This platform approach allows insurers, banks and digital brands to launch faster, expand across borders and deliver a better experience to their customers without having to build or maintain the insurance infrastructure themselves.

Benefits of insurance-as-a-service & digital insurance solutions for companies

Non-insurance companies are reaping the rewards of insurance-as-a-service models. It allows them to offer insurance without getting bogged down in all the nitty-gritty.

After all, insurance is a complex, regulated industry that requires specific licences, knowledge of country-specific laws and complicated setups when it comes to underwriting, pricing and risk management.

By partnering with an IaaS provider, brands can slot insurance into their current product or service, gaining a competitive advantage and becoming a one-stop-shop for their customers.

In fact, a BCG survey found that 65% of consumers would purchase embedded insurance from non-insurance brands when it’s integrated into the purchasing journey.

- Revenue from added value: create new revenue streams by embedding relevant protection alongside your core product or service.

- Faster time‑to‑market: launch insurance programs quickly, without the delays of building infrastructure or managing multiple partners.

- Higher customer satisfaction: offer protection at the right moment in the customer journey, creating a smoother experience that boosts loyalty and engagement.

- Better user experience: by partnering with IaaS providers rather than traditional insurers, you get digital subscription flows, streamlined claims processing and customer support – powered by AI and data.

- Differentiation in crowded markets: stand out from competitors by offering insurance tailored to your customers.

- Maintain control over your insurance experience: by working with an IaaS orchestrator, you can work with different product lines and risk carriers across markets. The orchestrator handles the complexities, so you can focus on your core business with digital insurance solutions.

.jpg)

Businesses can offer embedded insurance in two different ways: by natively embedding it within their product or service, or selling it as an add-on that complements their offer.

Many banks embed insurance within their payment cards or plans. The higher the tier, the better the insurance. Revolut Ultra is a good example of how digital insurance solutions can be bundled into premium banking plans with its top-tier cancel for any reason trip and event insurance.

An increasing number of brands and online platforms offer insurance as an add-on to their product, such as a car maker prompting customers to buy motor insurance with their new car or an airline asking customers to add travel insurance when booking a flight.

'Embedded insurance is not a totally new topic – we’ve always tried to take an embedded approach in our customer journey,’ says Andreas Glunz, Head of Insurance Business UK at BMW Group Financial Services. ‘But of course today’s technology has taken it to a new level because we can fully integrate it into our digital channels. From a customer perspective, we always want to offer a convenient, one-stop shop solution – a suitable insurance product at the right point in time. This means there are more product opportunities, which leads to new and improved revenue streams for us and an enhanced value proposition for customers.’

Benefits of insurance-as-a-service for insurers

For traditional insurers who have the insurance expertise, the rise of insurance-as-a-service opens the door to a more agile, modern way of doing business.

Many long-standing carriers face the challenge of legacy systems, manual processes and slow product cycles. Partnering with an IaaS platform lets them bridge that gap without overhauling their entire infrastructure.

- Faster product deployment: launch or adapt insurance programs in weeks instead of months by outsourcing development.

- Scalable growth: risk carriers are inherently local entities. IaaS allows expansion across markets and product lines more easily through a flexible, modular setup.

- Smoother distribution & better customer experience: deliver smoother digital journeys for customers or brand partners, boosting satisfaction and retention.

- Reduced operational complexity: rely on orchestration platforms to handle reporting, data exchange and integrations.

- Access to new distribution channels: partnering with an IaaS platform can open the door to new partnerships with non-insurance brands.

By partnering with an embedded insurance provider, insurers and brokers can digitise key parts of their value chain. This not only streamlines distribution but also allows them to reach new customer segments through brand partnerships. The result is improved efficiency, increased premium volumes and a stronger position in the market.

Technology-driven orchestration also reduces the operational burden for insurers. With reporting, data flows and pricing handled through the platform, insurers can focus on underwriting and risk management while still meeting the expectations of digital-first customers.

%202.png)

Benefits of insurance-as-a-service for consumers

Insurance is becoming readily available to consumers by being directly embedded within the digital ecosystems they already use.

For example: a banking customer might upgrade to a paid Revolut plan, which comes with purchase protection insurance for everyday spending. Or a customer might be prompted to add insurance to their cart while purchasing a flight online.

So rather than searching high and low for coverage post-purchase, customers find it's already offered at the right moment by the brands they know and trust.

In fact, 60% of online shoppers say insurance offered at checkout would increase their odds of making the purchase.

- A more seamless insurance experience: insurance is built directly into checkout flows and digital journeys, so customers don’t have to go looking for it.

- Relevant coverage: protection is based on your behaviour, interests or lifestyle.

- Usage-based pricing: pay only for the coverage you need, when you need it.

- More transparency: clear terms, simple language and better communication.

- Smarter support: faster claims and better customer service, powered by data and AI.

- Peace of mind: feel better about the purchases you make, knowing you’re covered if something goes wrong.

Why insurance-as-a-service is the next step for insurers, brands and consumers

As the world becomes more connected, so does the need for protection that matches the pace of our lives. Insurance-as-a-service is more than a digital upgrade; it’s a way to extend meaningful protection to more people, wherever they are.

For consumers, it means simple, relevant cover that’s available exactly when and where they need it. For brands, it creates fresh revenue streams and stronger customer loyalty by embedding relevant protection right into the experience. And for insurers, it’s a way to modernise operations, unlock new distribution channels and scale without the pain of rebuilding legacy systems.

The result is a business model that drives growth, strengthens relationships and brings us closer to a more seamless global safety net, where insurance is simple, accessible and embedded into the services we use every day.

If you’re ready to be part of this new era of insurance-as-a-service, get in touch.

.webp)

{kind=link}

{kind=link}